By Andreas Wocke | RiseOfMind.com

This is the third and final part of my series on working and doing business with Indian teams. Part 1 focused on location and corporate structures, whilst Part 2 covered recruitment, loyalty and employment law. Today, I’ll be looking at what makes India so significant in the long term – and what German companies really need to know in their day-to-day operations.

India and AI: More than just an extension

Just a few years ago, India’s role in the global tech ecosystem was clearly defined: execution, not necessarily innovation. Good engineers, low prices, reliable delivery. Today, this picture is only partially accurate.

According to the Stanford AI Index Report 2025, India ranks third globally in AI competitiveness and is the second-largest contributor to GitHub AI projects – behind the US, ahead of China. Cumulative private AI investment from 2013 to 2024 stood at around 11.1 billion US dollars; in 2024 alone, over US$780 million flowed into Indian AI start-ups – an increase of almost 40 per cent on the previous year.

The Indian central government has launched the IndiaAI Mission, a government programme with a budget of around US$1.2 billion. The aim: a sovereign AI infrastructure and proprietary large language models for Indian languages. The Bengaluru-based start-up Sarvam AI was selected in 2025 to develop India’s first government-backed LLM – trained on Hindi, Bengali, Tamil, Telugu and other languages. Krutrim, also from Bengaluru, became India’s first AI unicorn as early as January 2024.

For medium-sized companies with existing India Capability Centres, this means: Local talent is developing at a rapid pace. Anyone who currently has pure testing or backend teams in Bengaluru will find, in three to five years’ time, that the same employees have built up serious AI expertise. This is an opportunity – provided it is recognised early enough and roles are developed accordingly.

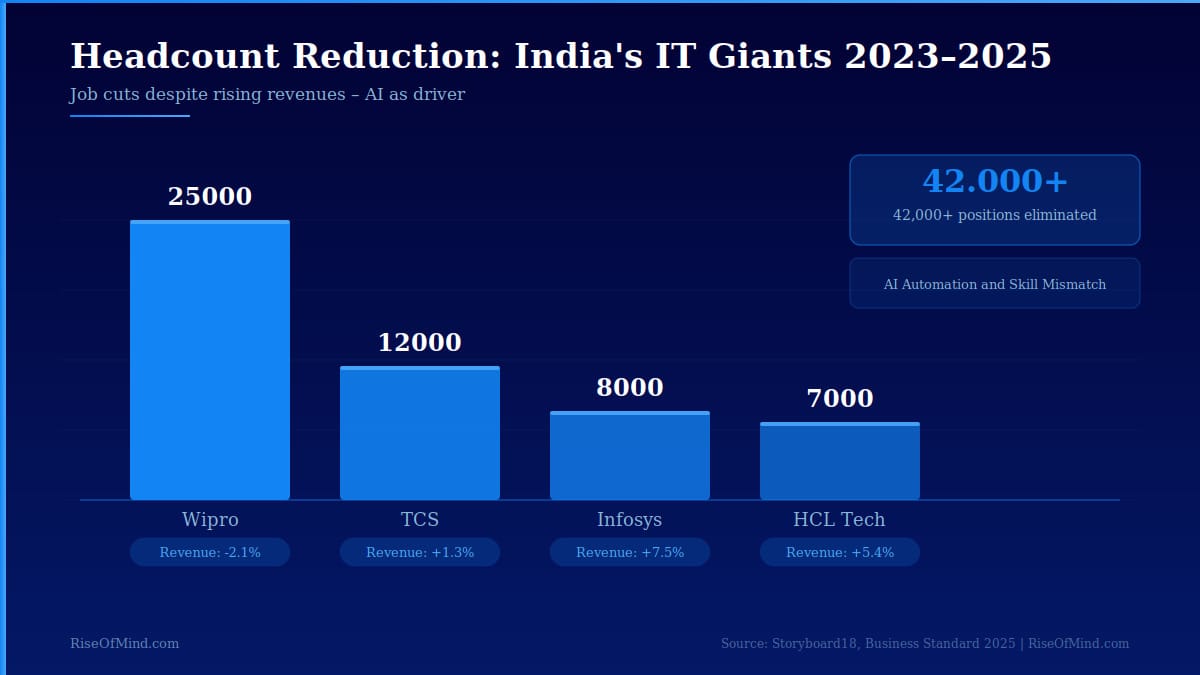

The structural shift: When IT giants cut their developer headcount

Anyone wishing to understand where the Indian IT market is heading must keep an eye on an uncomfortable trend: the major Indian IT service providers are slashing their workforce – of all times, just when their revenues are stable or growing.

According to Storyboard18, TCS, Infosys, Wipro and HCL Tech have collectively reduced their workforce by over 42,000 jobs over the past two years. TCS also announced the loss of a further 12,000 jobs – around 2 per cent of its total workforce, predominantly in middle and senior management. Wipro recorded the sharpest decline, with over 25,000 jobs lost. And this despite revenues rising by 1.3 per cent at TCS and 7.5 per cent at Infosys over the same period.

The companies’ reasoning is clear: skill mismatch and AI automation. TCS CEO K. Krithivasan spoke of “limited deployment opportunities and skill mismatch”. Wipro has over 200 AI-powered “intelligent agents” in use across HR, finance and legal, and is investing one billion US dollars in AI over three years. According to a Jefferies report, clients are actively demanding that service providers deliver the same work with fewer staff – AI costs are being built into pricing models.

The traditional Indian IT model was based on a single value proposition: Indian developers cost a fraction of their Western counterparts. It is precisely this approach that is being systematically undermined by AI coding assistants and automation. The World Economic Forum forecasts that by 2027, AI will eliminate 83 million jobs worldwide and create 69 million new ones – a net loss of 14 million jobs.

What does this mean for European companies? Paradoxically, it is good news for operators of their own India Capability Centres. Job cuts at the major outsourcing providers mean that experienced, highly qualified IT professionals are entering the market – people with enterprise experience who were previously tied to stable large corporations. The recruitment window for self-managed subsidiaries is particularly favourable right now.

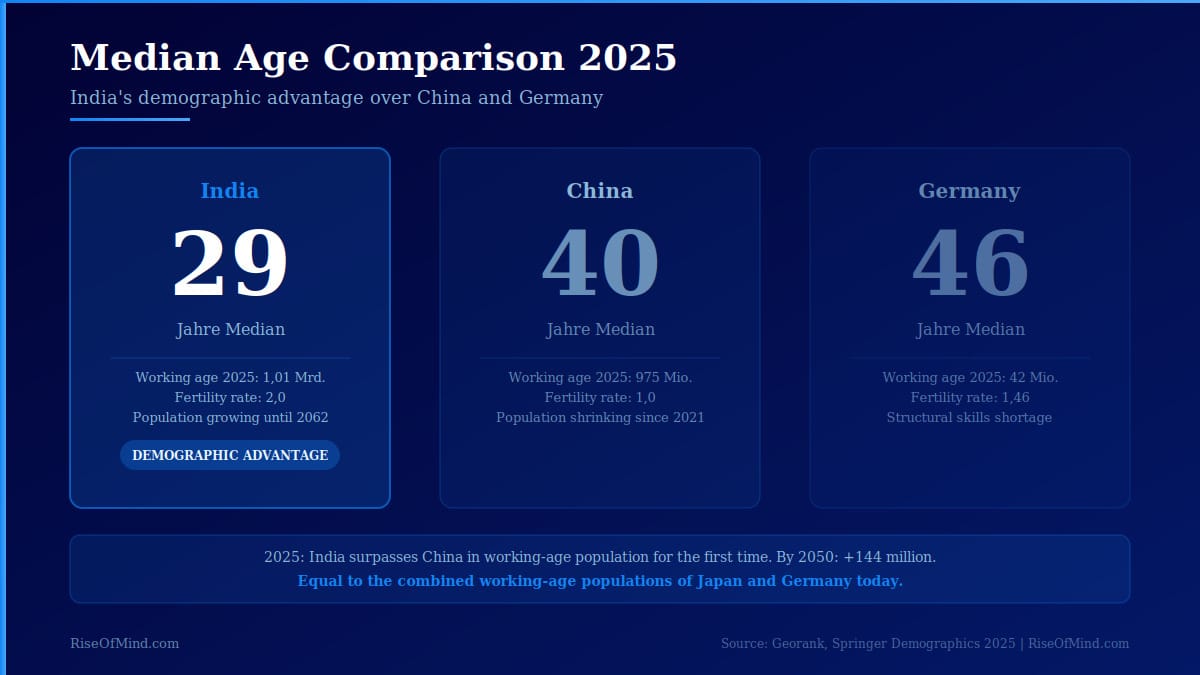

The demographic foundation: Why India is not China

There is one key figure that explains everything: the median age. In India, it will be under 30 in 2025. In China, over 40. In Germany, around 46.

China is shrinking – India is growing

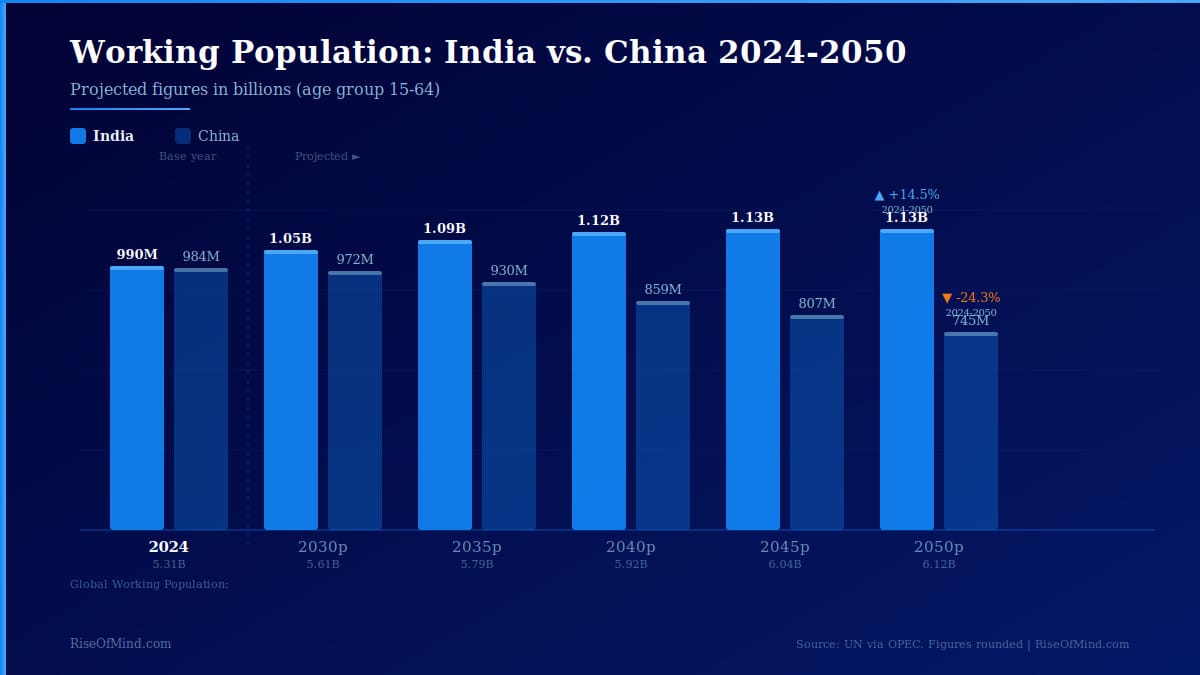

Since 2021, China has been experiencing a continuous decline in population. The fertility rate has fallen to below one child per woman, and the proportion of people aged over 65 is already just under 15 per cent – more than twice as high as in India, at around 7 per cent. In 2025, India will have more people of working age than China for the first time: over one billion compared to 975 million. By 2050, this figure will rise to 1.13 billion – an increase of 144 million, exceeding the combined current working-age populations of Japan and Germany.

I have observed this since my first visits in the early 2000s. Back then, the demographic advantage was still abstract – a figure in reports, a curve in forecasts. Today, you see it every day in the offices of Bengaluru: young faces wherever you look.

Two challenges are holding back this potential: the skills gap (according to the India Skills Report 2024, only 52 per cent of university graduates are considered ready for the labour market) and the low female labour force participation rate, one of the lowest in the world. The demographic dividend is real – but it needs to be worked for.

Understanding culture: What really matters

Cultural misunderstandings rarely arise from malicious intent – almost always from differing assumptions about what is taken for granted.

Hierarchy and the art of the indirect ‘no’

Indian companies have a strongly hierarchical structure – deeper than the organisational chart suggests. In a meeting, an Indian employee will rarely contradict their superior, and certainly not in public. It is a matter of ‘saving face’. The result: problems are not escalated, and a firm ‘no’ is rarely heard. ‘I’ll try’ sometimes means ‘actually not feasible, but I don’t want to disappoint anyone’.

The solution does not lie in demanding directness, but in creating a communication environment in which problems can be addressed safely – ideally in a one-to-one conversation. Scope for action must be explicitly delegated: what sounds self-evident to Germans is a genuine empowerment for many Indian colleagues.

Festivals, public holidays and religion as planning factors

In addition to three national public holidays, there are between 8 and 14 further ones depending on the state – many of them based on the lunar calendar, meaning they fall on different dates each year. Diwali and Holi are non-negotiable: around these festivals, employees visit their families, often for several days. Anyone setting important deadlines shortly before Diwali is bound to be disappointed.

Recommendation: Agree on a holiday calendar together at the start of the year. Religion also influences business life more strongly than in Germany – the signing of a contract may be postponed because the timing is considered unfavourable according to the lunar calendar. Respecting this opens doors.

Customs and imports: What can you bring into India?

For companies importing products into India – measurement technology, machinery, specialist equipment – the customs system is a significant cost factor. The Basic Customs Duty (BCD) is 15–20 per cent for electronics and typically between 5 and 15 per cent for machinery. Added to this is the Integrated GST (IGST), usually 18 per cent of the goods’ value plus BCD – effectively resulting in 25–40 per cent duties on the goods’ value. This is no coincidence, but part of the plan: the ‘Make in India’ strategy systematically favours local manufacturing.

Recommendation: engage a local customs and logistics consultant. The ICEGATE portal is well structured digitally, but the finer points require on-the-ground expertise. Important to note: as things stand, used equipment cannot be imported into India. Anyone requiring hardware locally – as a demo unit or for software development – must have new goods delivered from Germany.

Conclusion: India is not a sprint – it is a long-distance race

After more than 15 years working with Indian teams, I have learnt one thing: those looking for quick wins will be disappointed. Those who view India as a long-term strategic partnership will be rewarded. The demographic fundamentals are exceptional, the AI boom is real, and the cultural differences can be overcome – not through assimilation, but through mutual understanding.

Invest in relationships, not just contracts. A local contact whom you trust and, ideally, have known for years is worth more than the most sophisticated service level agreement.

The skills shortage in Germany and Europe is structural, not cyclical. India is one of the few credible answers to this – not as a cheap solution, but as a long-term strategic partnership with a country that is growing demographically, catching up technologically and is determined to work with European companies.

Those who open this window today will have a significant head start tomorrow.

Sources

- Stanford AI Index Report 2025 – https://aiindex.stanford.edu

- Observer Voice: India Accelerates AI Growth (Feb. 2026) – https://observervoice.com/india-accelerates-ai-growth-with-major-investments-and-initiatives-182949/

- Inc42: Indian GenAI Startup Tracker – https://inc42.com/startups/indian-genai-startup-tracker/

- Business Standard: India's share of global AI funding (Feb. 2026) – https://www.business-standard.com/markets/news/india-s-share-of-global-funding-pie-in-ai-stands-at-0-6-shows-data-126021901360_1.html

- Storyboard18: TCS, Infosys, Wipro and HCL Tech headcount reduces by 42,000 (Jul. 2025) – https://www.storyboard18.com/how-it-works/tcs-infosys-wipro-and-hcl-tech-headcount-reduces-by-over-42000-in-two-years -77264.htm

- Business Standard: TCS, Infosys continue staff layoffs even as revenue rises (Jul. 2025) – https://www.business-standard.com/industry/news/tcs-infosys-lay-off-indian-it-sector-job-cuts-automation-ai-reskilling-125072800505_1.html

- SME Futures: When AI came for the IT crowd – TCS's 12,000 redundancies (Jul. 2025) – https://smefutures.com/when-ai-came-for-it-crowd-inside-tcss-12000-layoffs-and-new-face-of-tech-employment/

- Policy Circle: AI disruption – TCS, Wipro layoffs underline skills deficit (Aug. 2025) – https://www.policycircle.org/industry/tcs-layoffs-ai-driven-economy/

- Visual Capitalist: India vs. China Working Age Populations 2024–2050 – https://www.visualcapitalist.com/charted-india-vs-china-working-age-populations-2024-2050/

- Georank: Age Demographics China vs India 2025 – https://georank.org/demographics/china/india

- Springer: The Demographic Race between India and China (2025) – https://link.springer.com/article/10.1007/s11113-025-09966-y

- Crossculture Academy: Cultural Differences in India – https://crossculture-academy.com/de/kulturelle-unterschiede-indien/

- Noventum Consulting: IT outsourcing to India – culture shock? – https://www.noventum.de/de/it-management-consulting/nc360-artikel/it-outsourcing-nach-indien-kulturschock-garantiert.html

- IndiaConnected: Holiday Entitlement and Public Holidays in India – https://www.indiaconnected.de/news-artikel/urlaubsanspruch-und-feiertage-in-indien-ein-leitfaden-fuer-arbeitgeber/

- India Briefing: Customs Duty and Import-Export Taxes in India – https://www.india-briefing.com/doing-business-guide/india/taxation-and-accounting/customs-duty-and-import-export-taxes-in-india

About the Author